Coatue

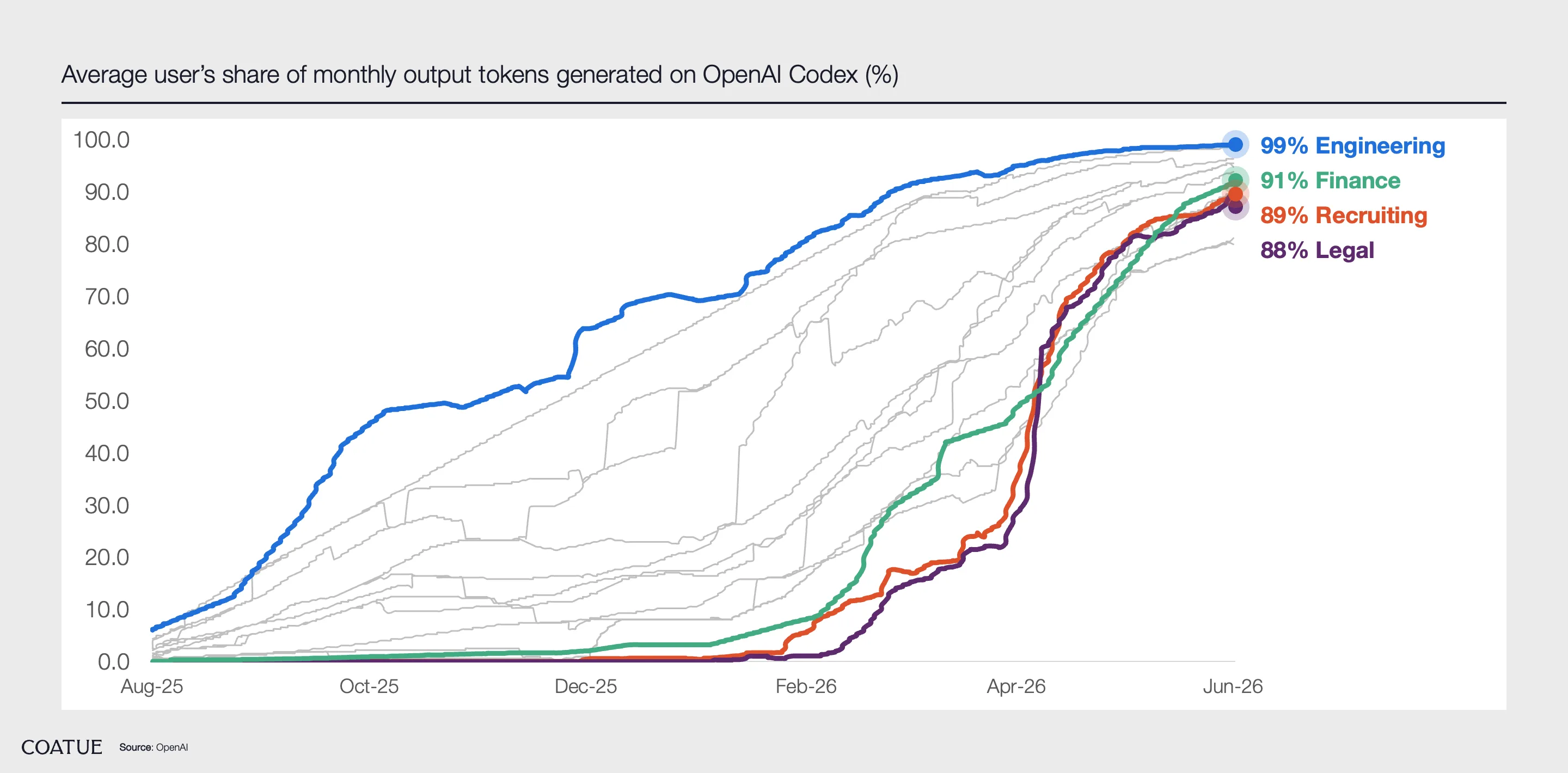

Codex adoption has broadened from engineering into nearly every function across OpenAI. Is this a predictor for the rest of the enterprise world?

Quick takes on trends driving markets

Codex adoption has broadened from engineering into nearly every function across OpenAI. Is this a predictor for the rest of the enterprise world?

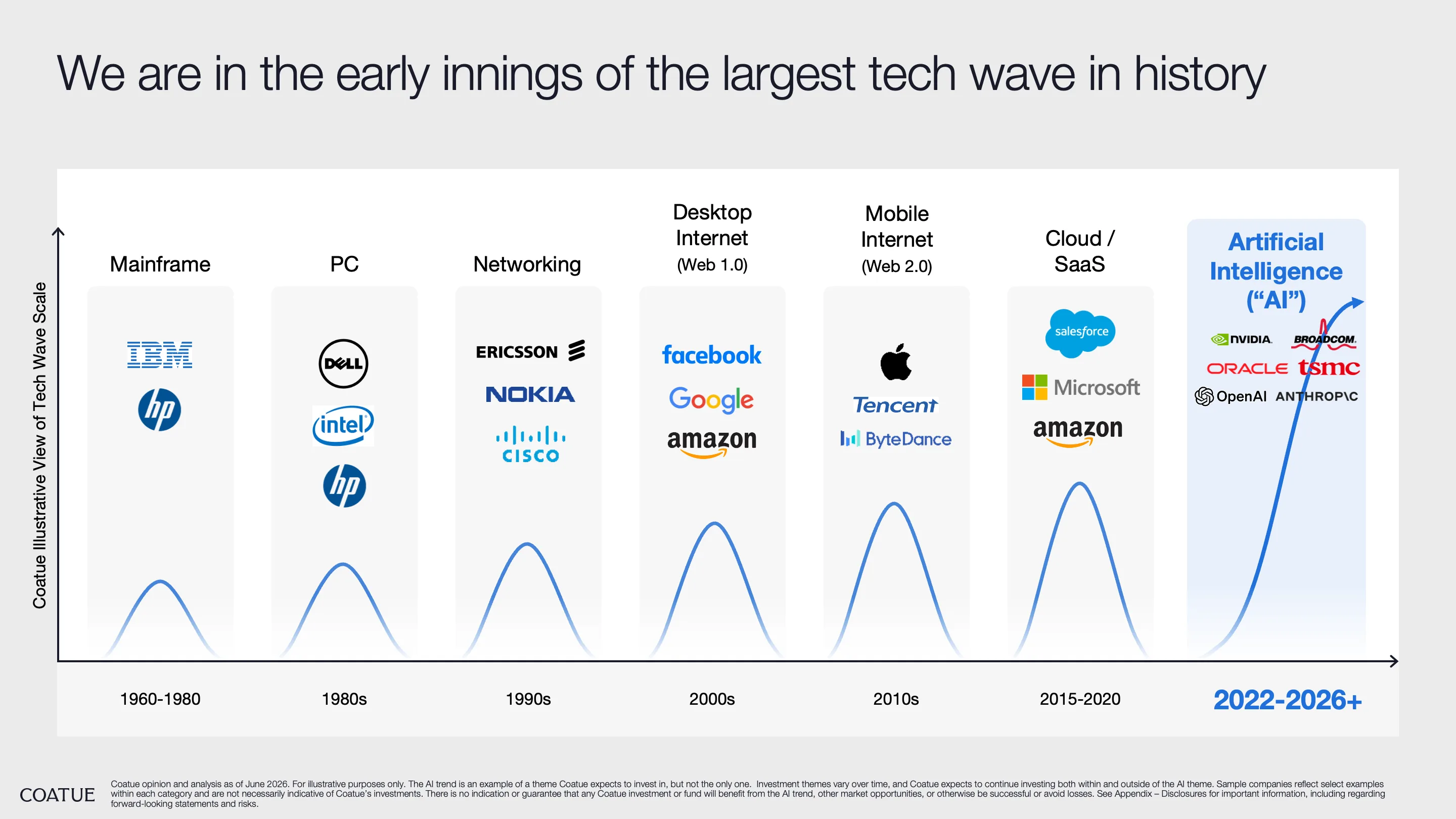

We spend a lot of time thinking about the big waves of technology, the move from mainframe to PC, the networking of those PCs, web 1.0 and web 2.0, SaaS, and now AI.

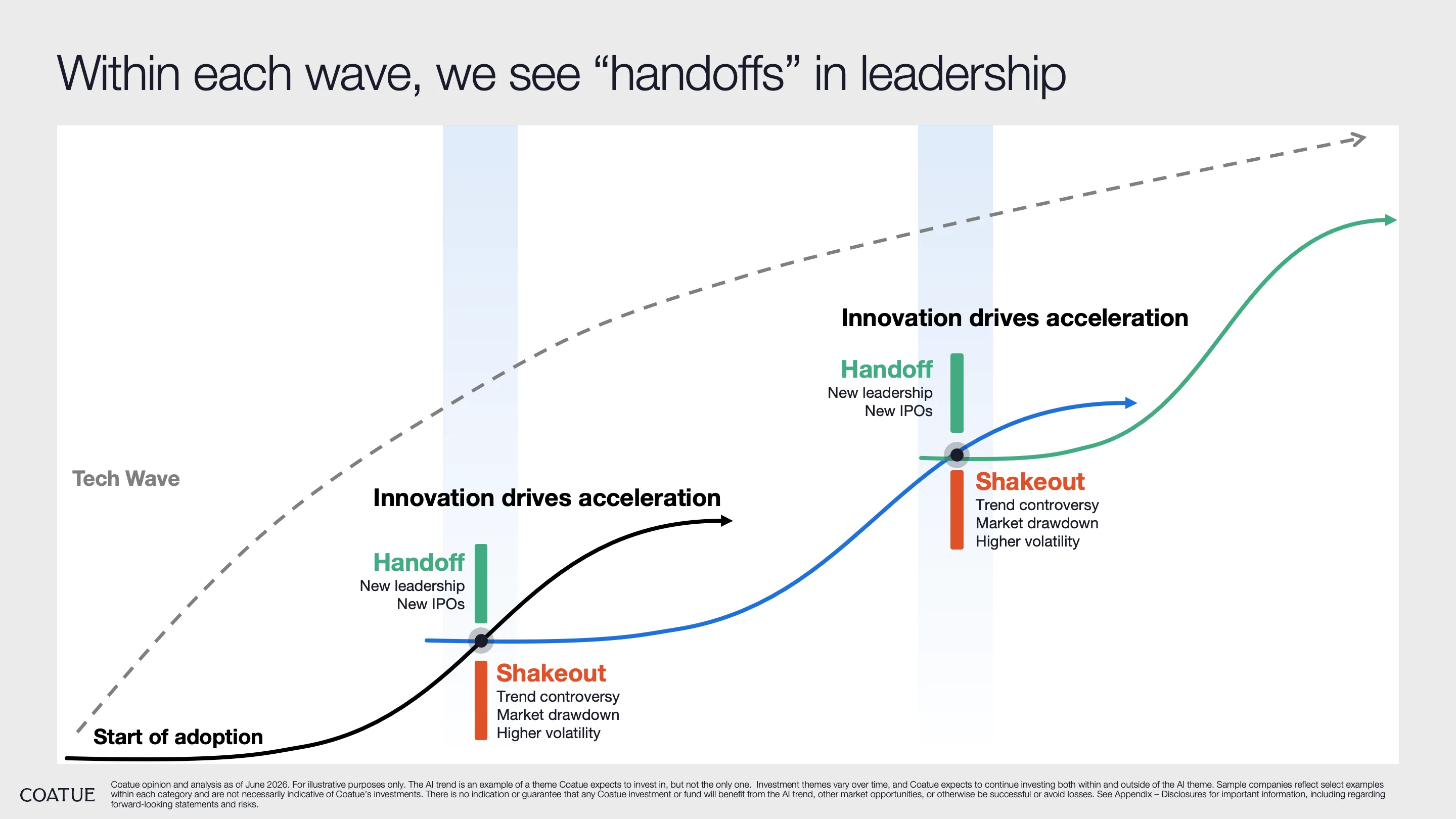

What is easy to miss is that inside every one of those waves are smaller waves. We call them handoffs, or shakeouts, and they tend to follow a recognizable pattern: new IPOs start appearing, more private companies form, drawdowns get sharper, and the whole market turns more volatile. By the time it settles, the companies sitting on top are rarely the same ones that led going in.

That raises the obvious question of whether software is in one of these handoffs right now.

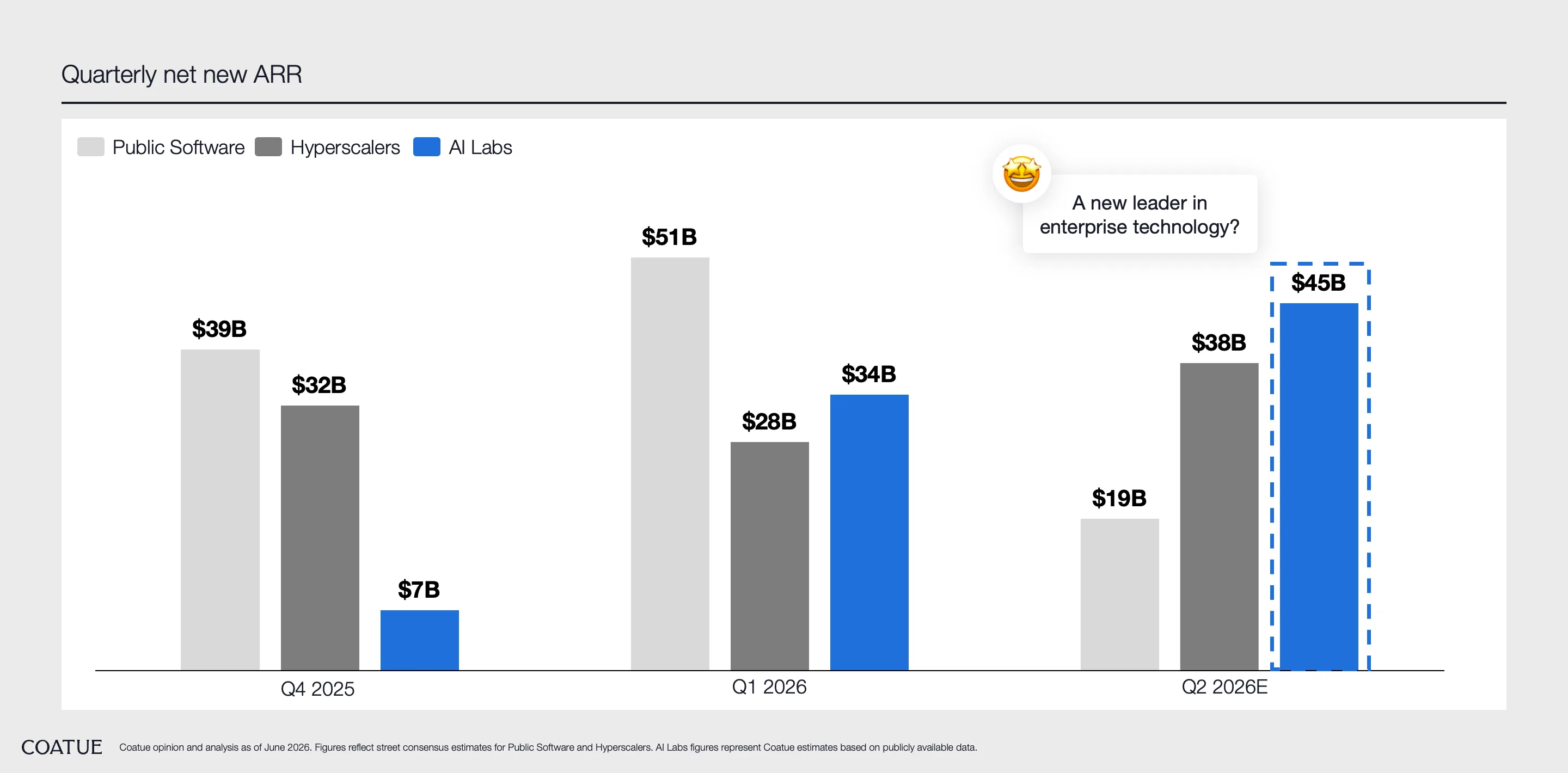

If you look at quarterly net new ARR, the AI labs are starting to out-add both the hyperscalers and the entire public software universe. When a new set of entrants is putting on more revenue than the incumbents that have defined the category for years, that is usually what the early stage of a handoff looks like.

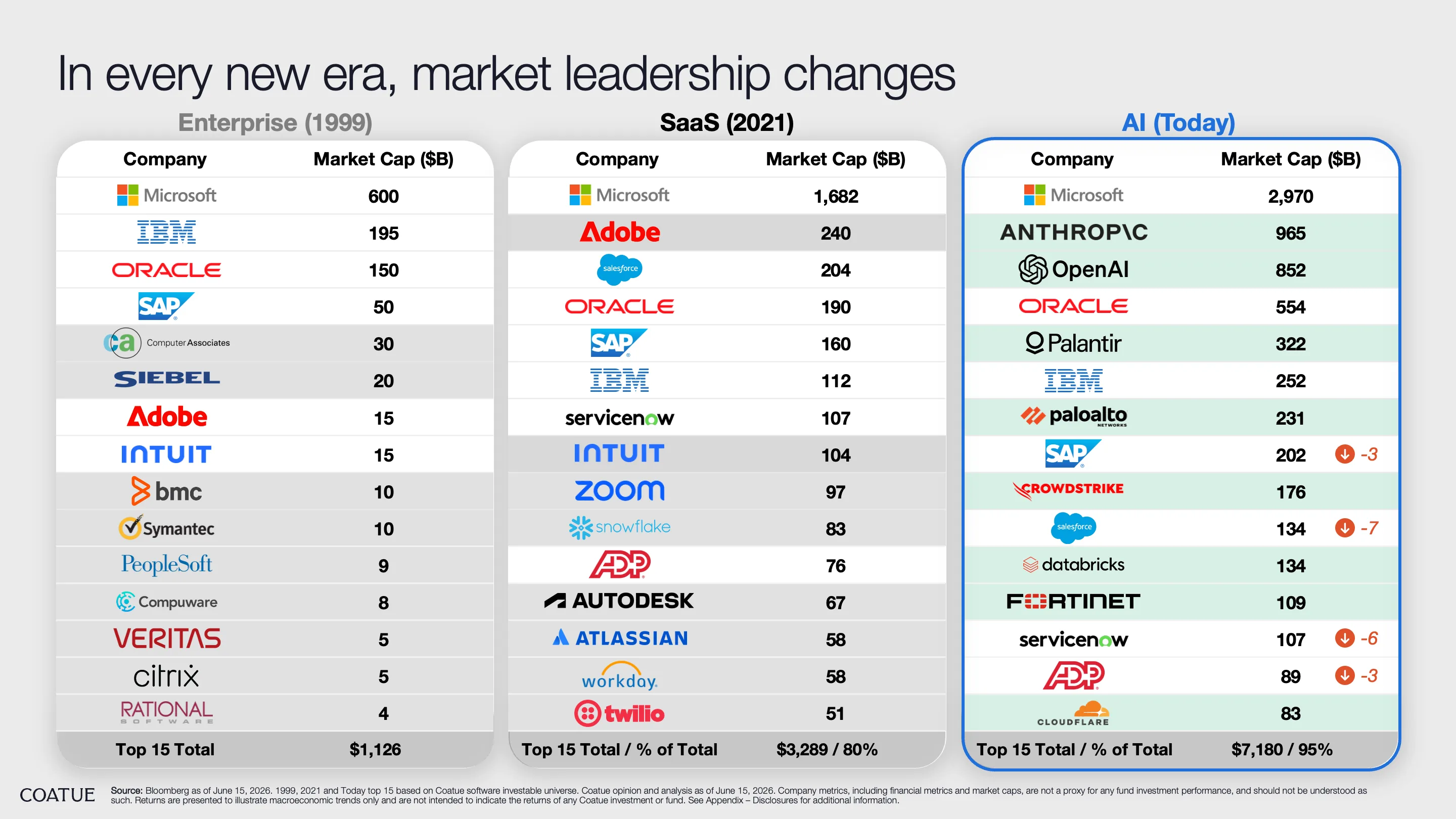

History suggests the leadership board gets redrawn each time this happens. When software moved from the enterprise era into SaaS, only a handful of the largest names carried over into the next list, and the companies now leading the AI era, OpenAI and Anthropic among them, did not even exist during the last shakeout.

For more on this C:\Take, watch Max:

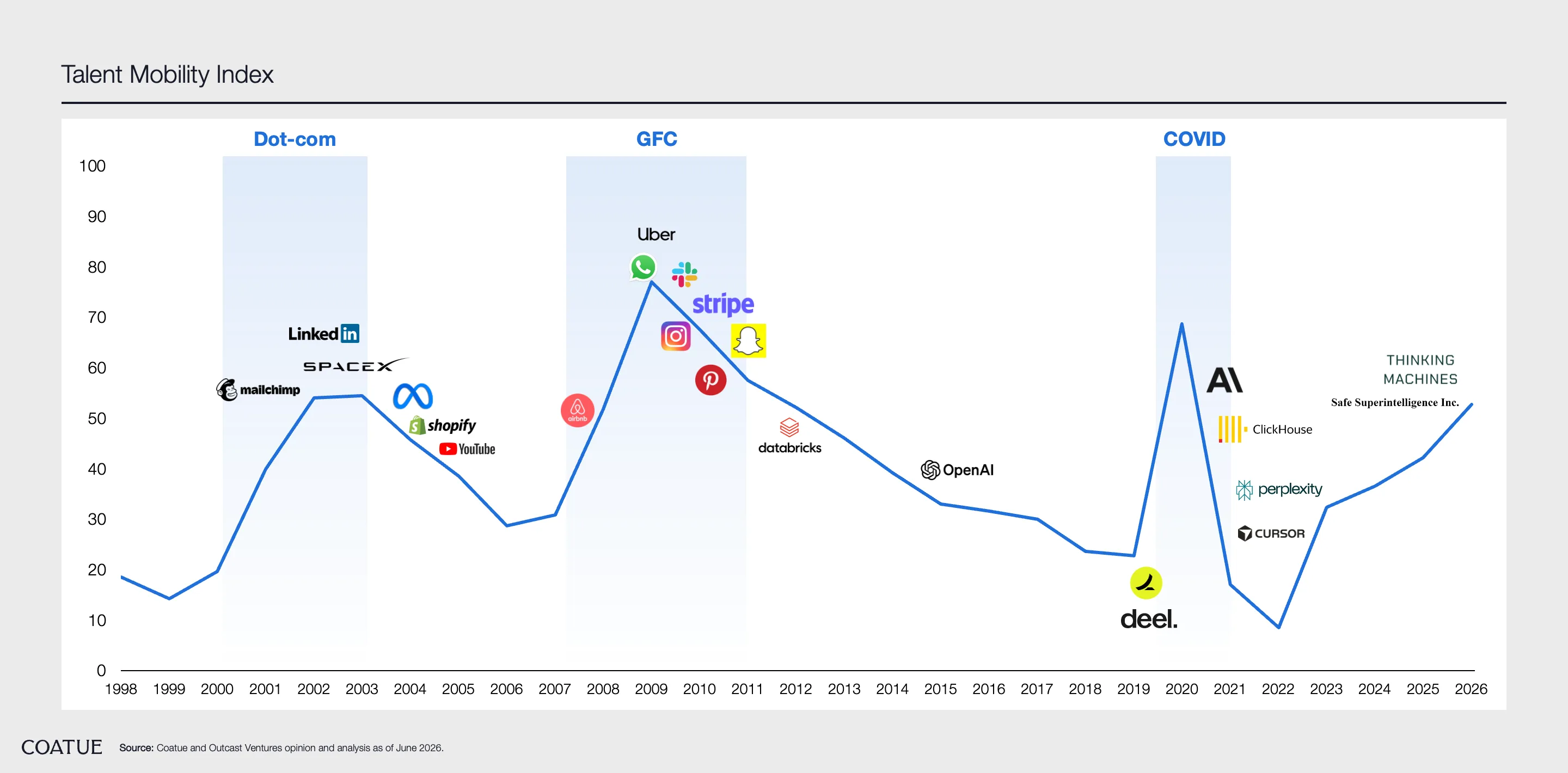

Innovation waves get credited to new technology. The real trigger is when great talent becomes available to build.

The Talent Mobility Index tracks how freely top tech talent can move in a given year, blending hiring, job change, and AI funding data into a single score.

The AI labs concentrated the best builders in the world and created extraordinary success. Now, as that success matures, some of those builders are stepping out to start what's next.

Data collaboration with Outcast Ventures and Coatue.

Is the baton passing? AI Labs are projected to generate the most net new ARR in Q2.

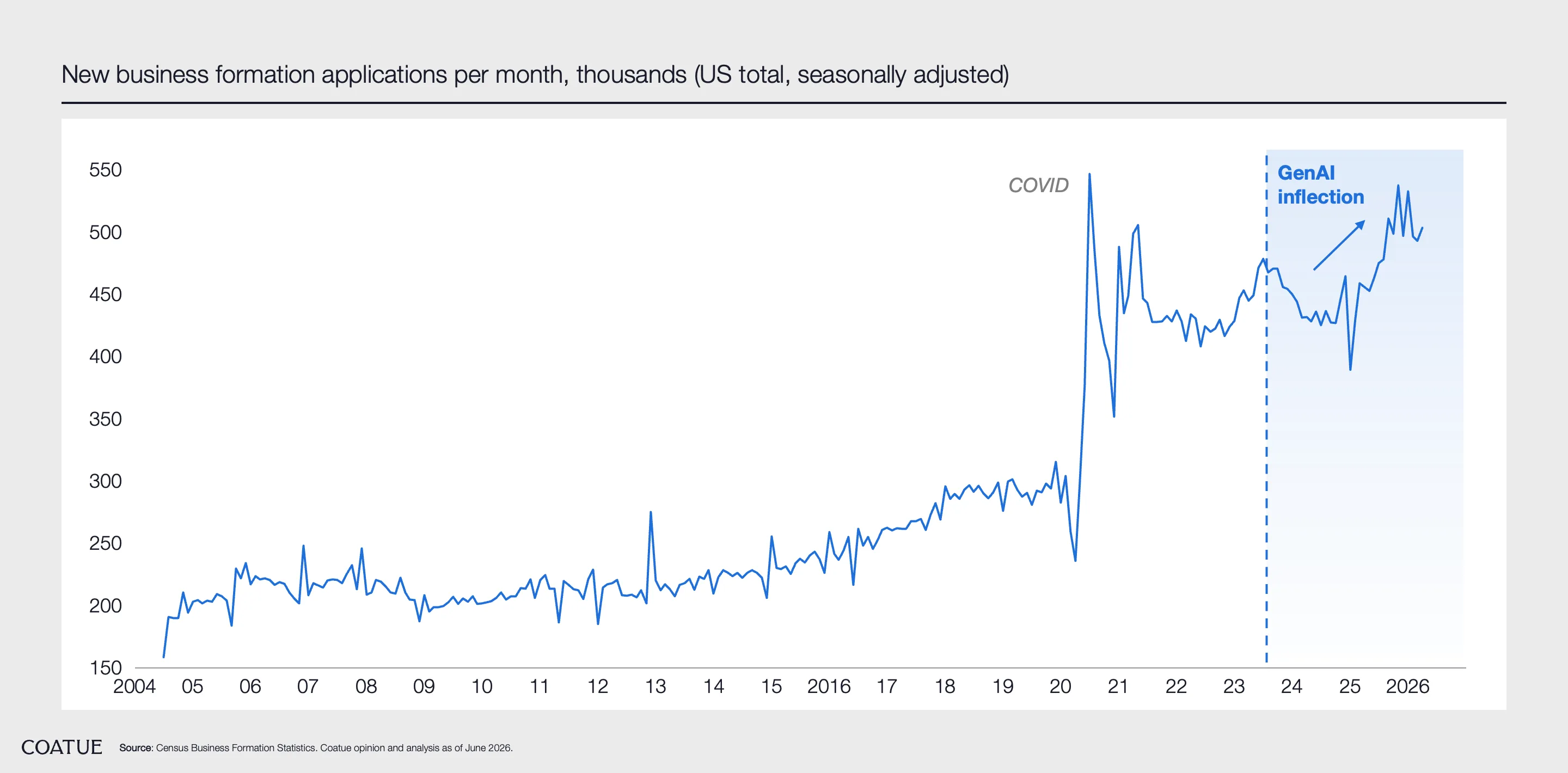

New business formation is inflecting! GenAI might be the catalyst.

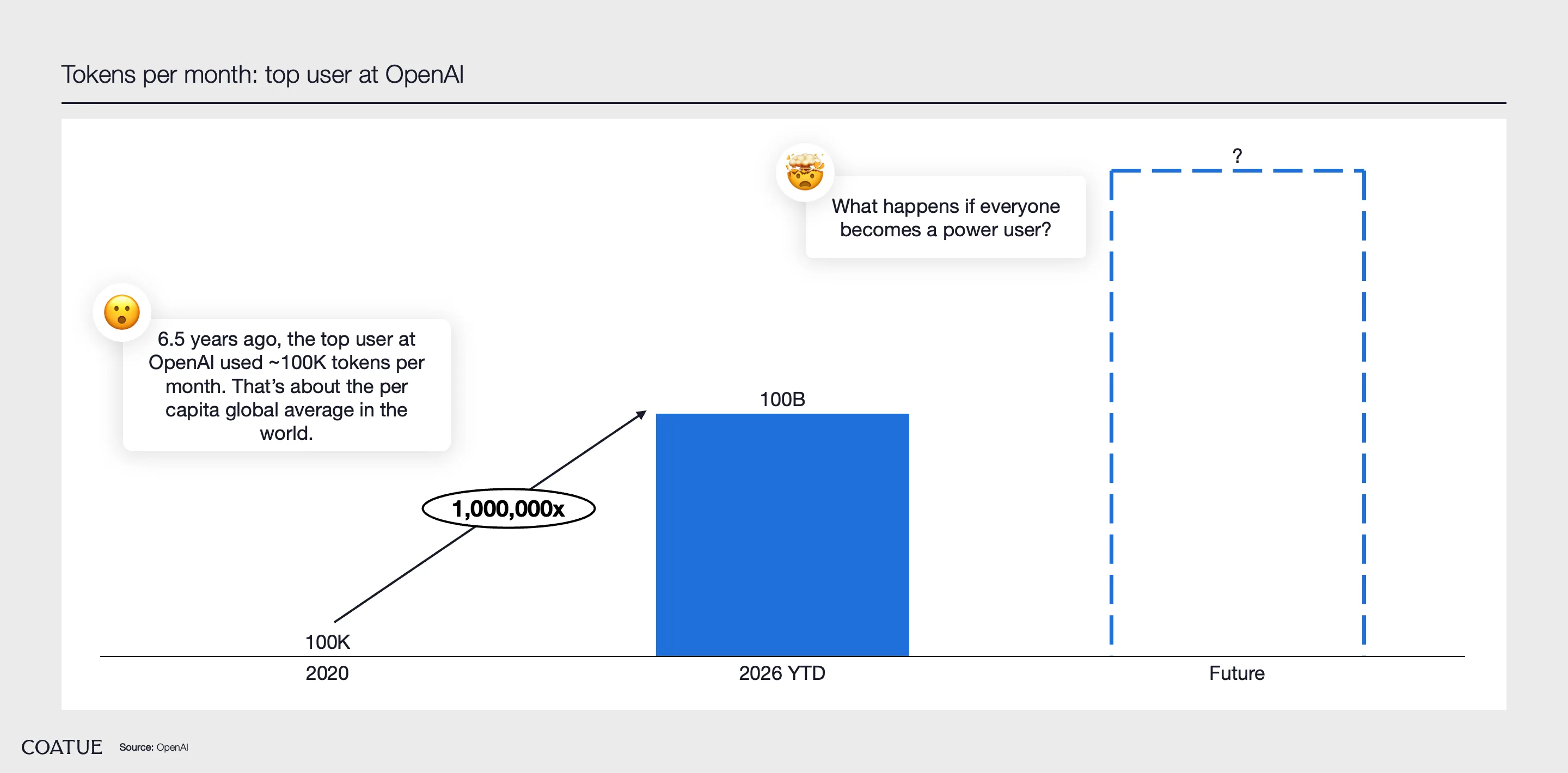

"What if it increases another 6.5x from here? We don't have anywhere near what's needed in terms of the infrastructure to support that."

- Sam Altman, OpenAI

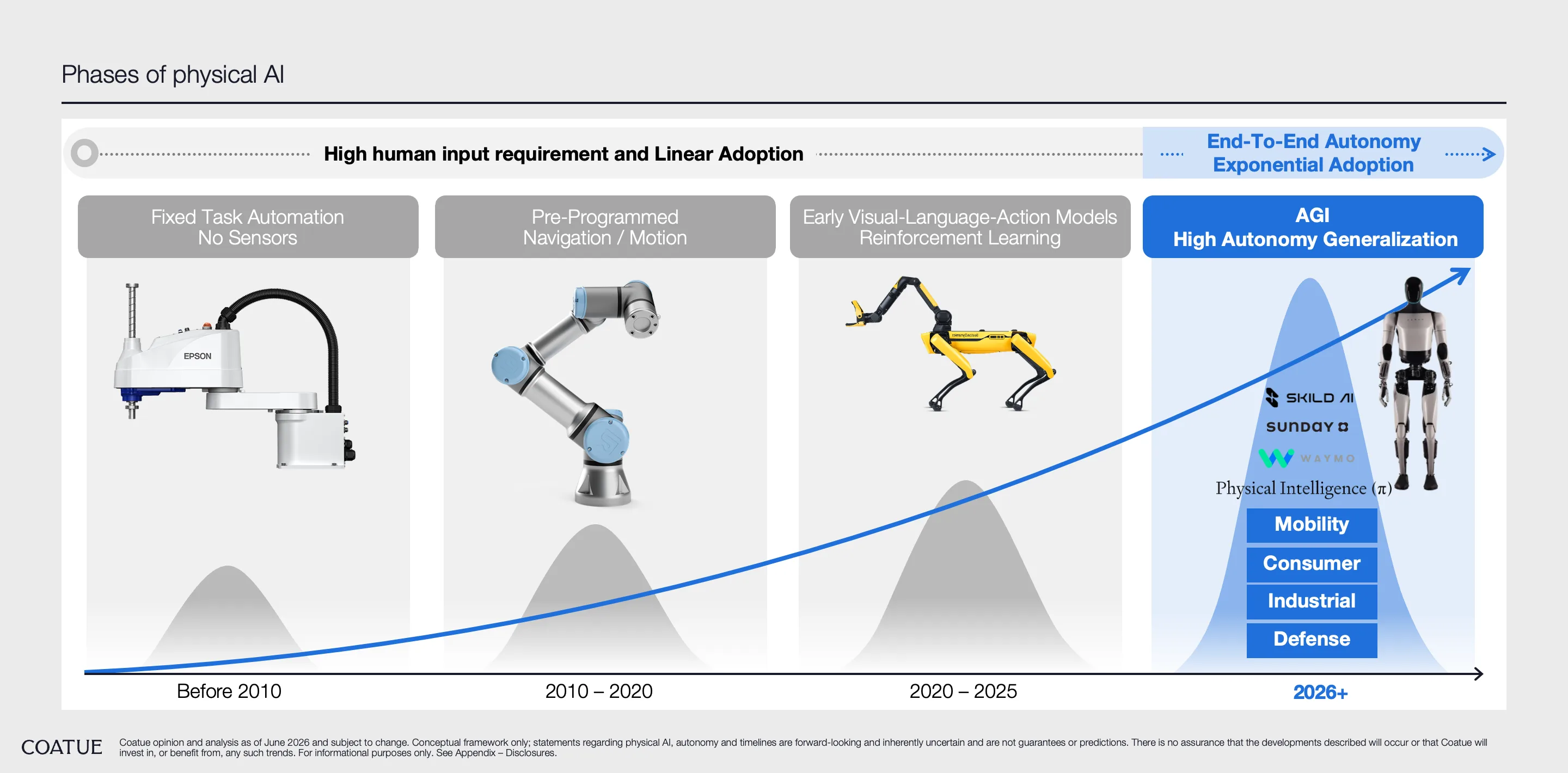

AI is entering a new phase: moving beyond digital tools and into fully autonomous systems operating in the physical world.

From advanced manufacturing and surgical robotics to robots in the home, the next wave of innovation will be defined by machines that can perceive, decide, and act in real-world environments. As AI escapes the screen, a new generation of companies is emerging to build the infrastructure, products, and platforms powering this shift.

For more on this C:\Take, watch Lucas:

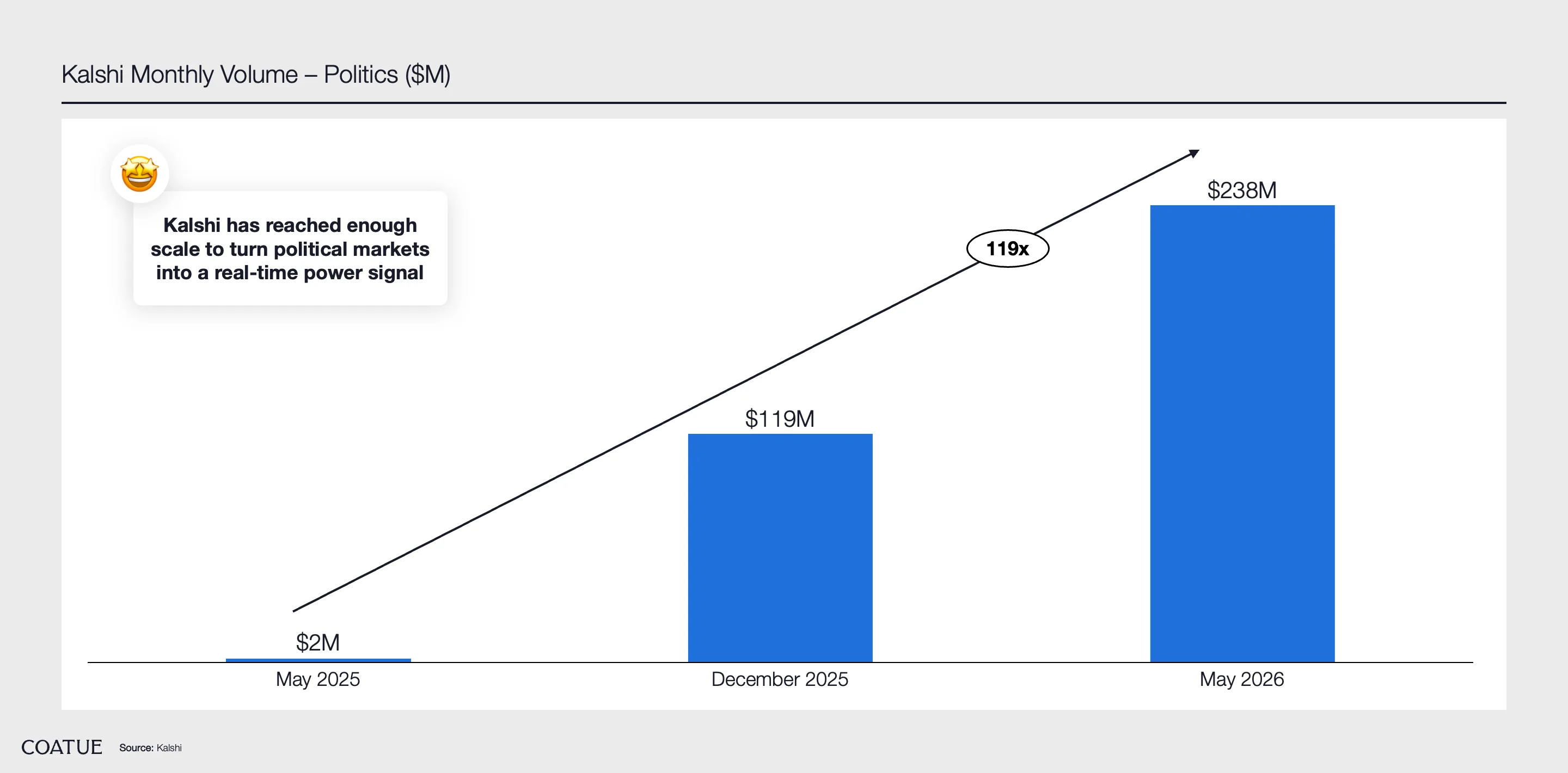

Kalshi's political volume has scaled dramatically, and the American Power Index (KPOW) is what that scale enables: a single-number gauge of the current balance of political power and where markets expect it to move, which Kalshi bills as an "S&P 500 for politics."

Products like this are paving the way for institutional adoption: a continuously updated context read on the political backdrop that could be overlaid against equities or policy-sensitive areas to track correlations rather than traded directly.

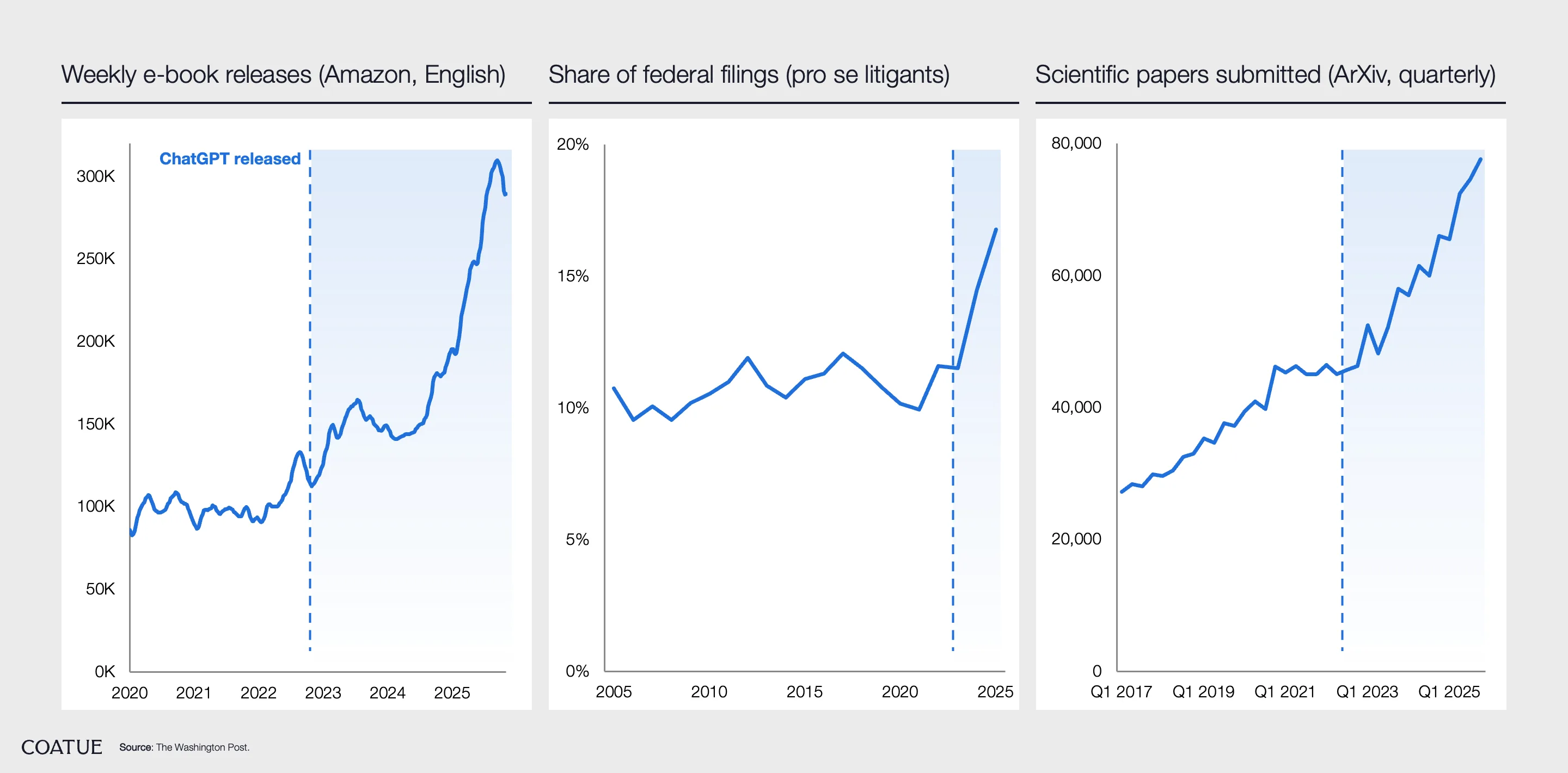

AI is bending the knowledge production curve across multiple domains.

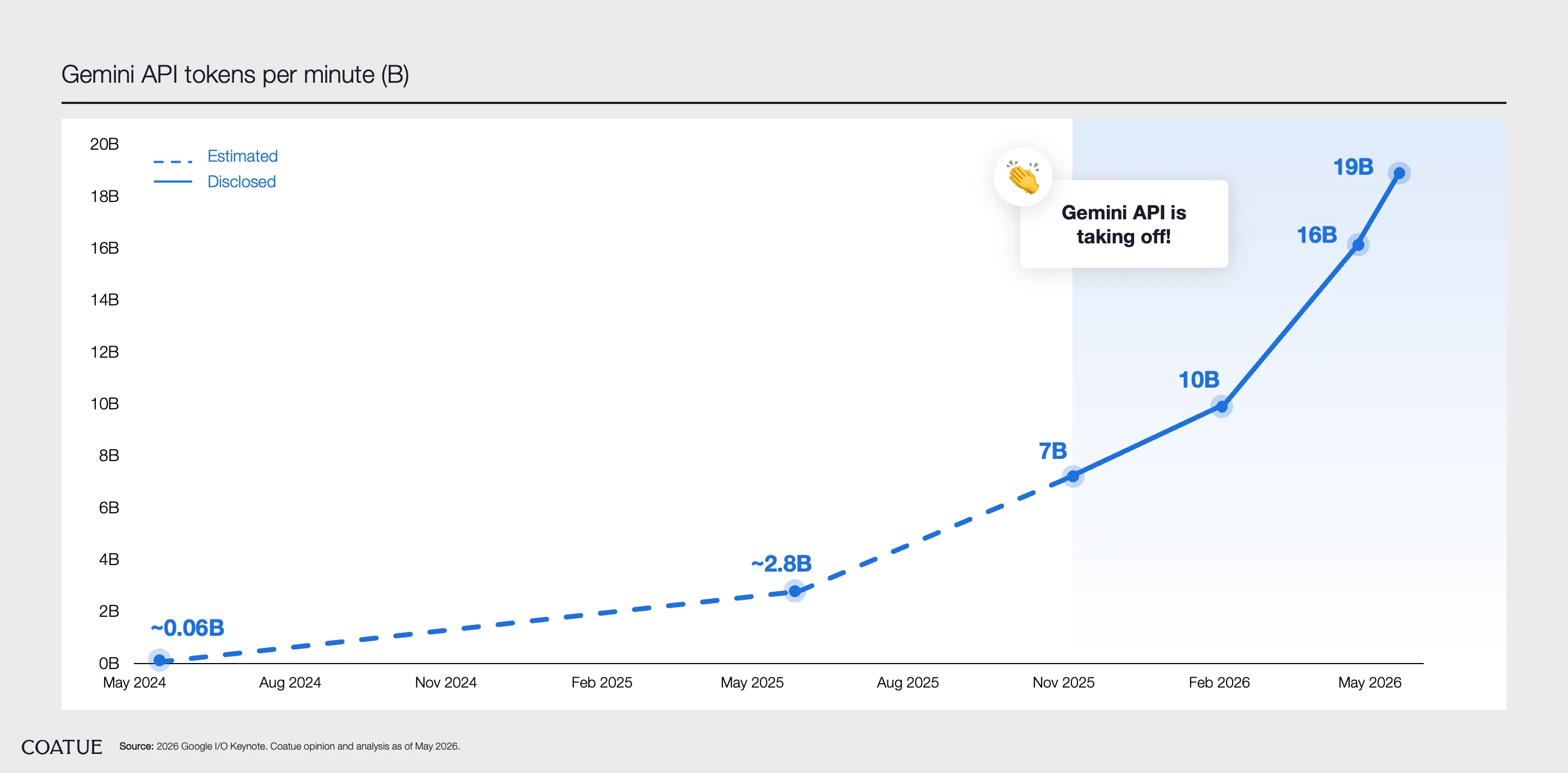

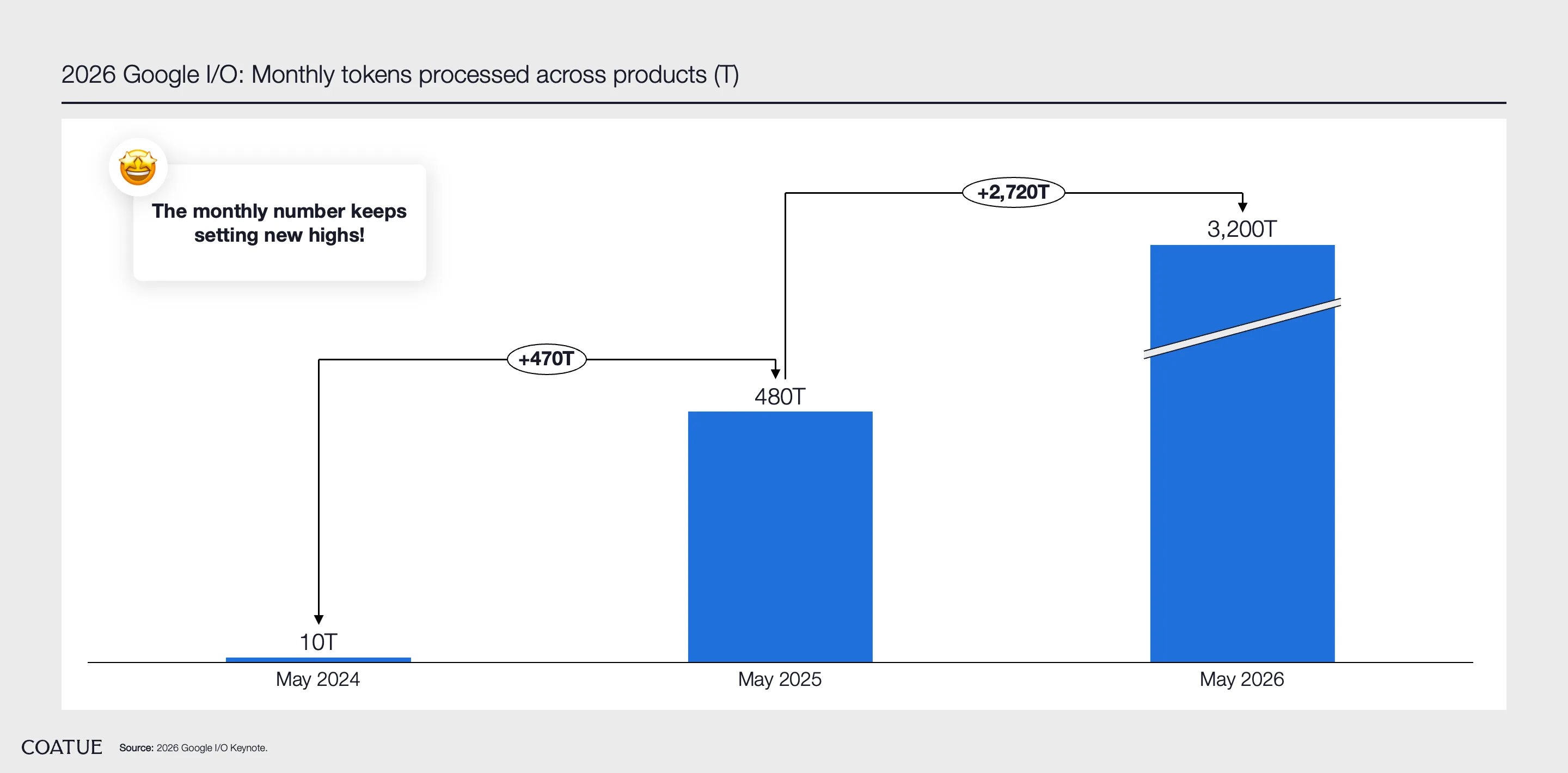

Earlier this week, we posted about Google's token count taking off across products. Looks like API demand is no different.

A year ago, it was 480T. Today it's 3.2Q! Tomorrow's chart might need a new unit of measurement.

Subscribe for the monthly LinkedIn newsletter