Jason Kahn

Some believe market valuations are highly predictive of forward returns. We’re skeptical.

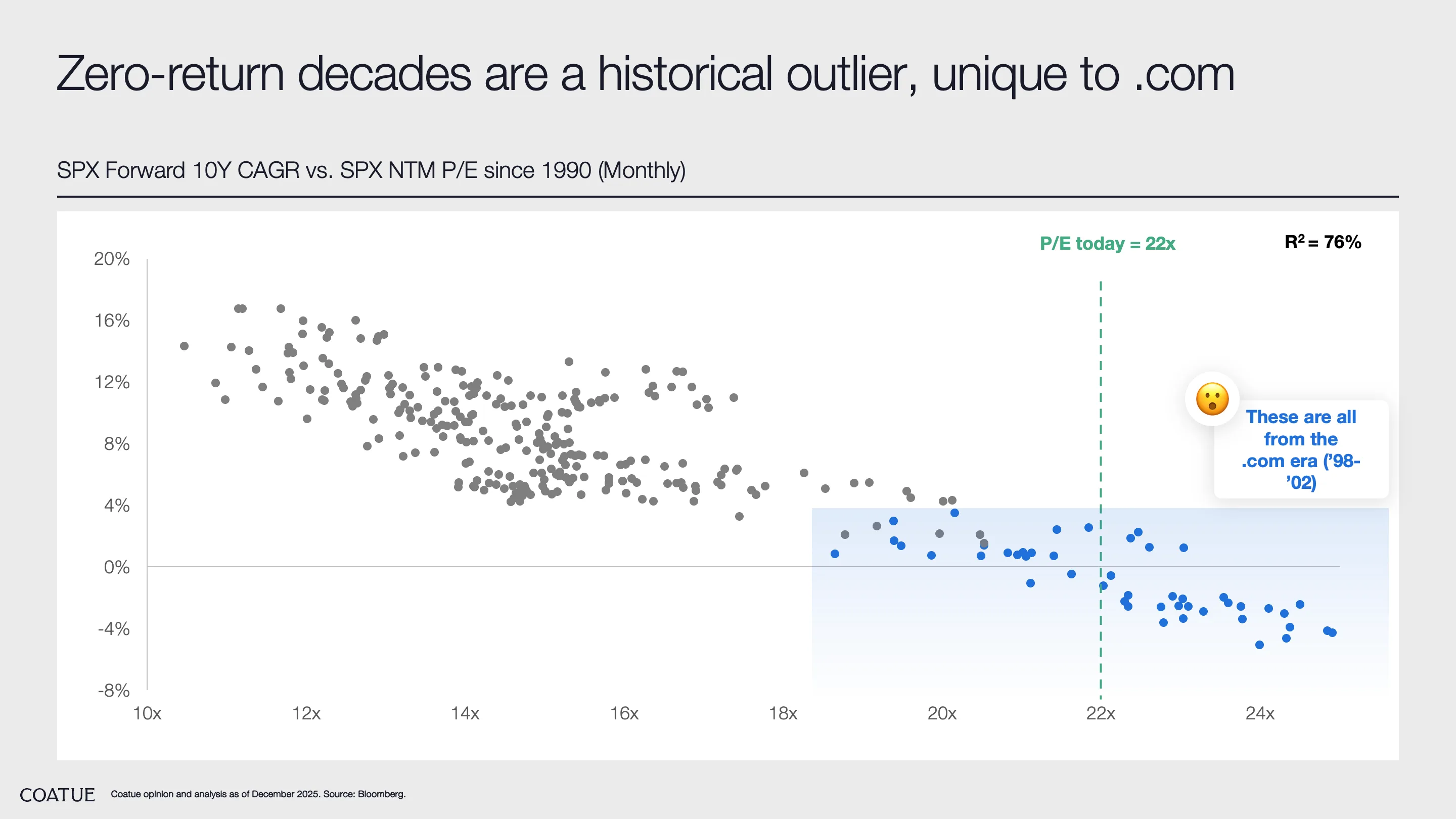

A chart circulating widely online suggests we may be in for a zero-return decade. We had reservations about the analysis, which focused on the historical relationship between the S&P 500 P/E ratio and subsequent 10-year forward returns.

In our own work, we found the underlying data to be heavily influenced by a single extreme outlier: the dot-com era from 1998-2002. Viewed through a broader lens, the data suggest that valuation levels alone are a far weaker predictor of long-term returns than the chart implies.

For more on this C:\Take, watch Jason:

Latest Takes